You’re Having a Baby! Keep These 7 Things in Mind

Ready to talk to an expert?

Your will.

A will isn’t just about handling your financial assets in the event of your death. It can also determine who will care for your child. Writing or updating your will with that information could be the most important pre-birth decision you make.

Your life insurance policy.

Your child will depend on you, and raising him or her could cost you $250,000. Life insurance is a way to help secure your child’s financial situation in the event of an accident. You may also want to consider a small policy for your child. In the very unfortunate event that your child passes away, a life insurance policy can help cover the potentially significant funeral expenses. Also, locking in life insurance for a young child now can make it possible for him or her to get more insurance later if the policy has a guaranteed insurability rider.

Your emergency cash fund.

Hopefully, you already have a fund to cover at least six months of expenses. But remember that with a baby, those expenses will grow to include things like diapers and daycare. Consider padding your emergency fund accordingly.

Your budget.

A child means big changes for your budget, especially if one spouse gives up part of his or her income to stay home with the child. As a way to help you plan, talk to the parents of a two-year-old to find out what you really need for your new baby.

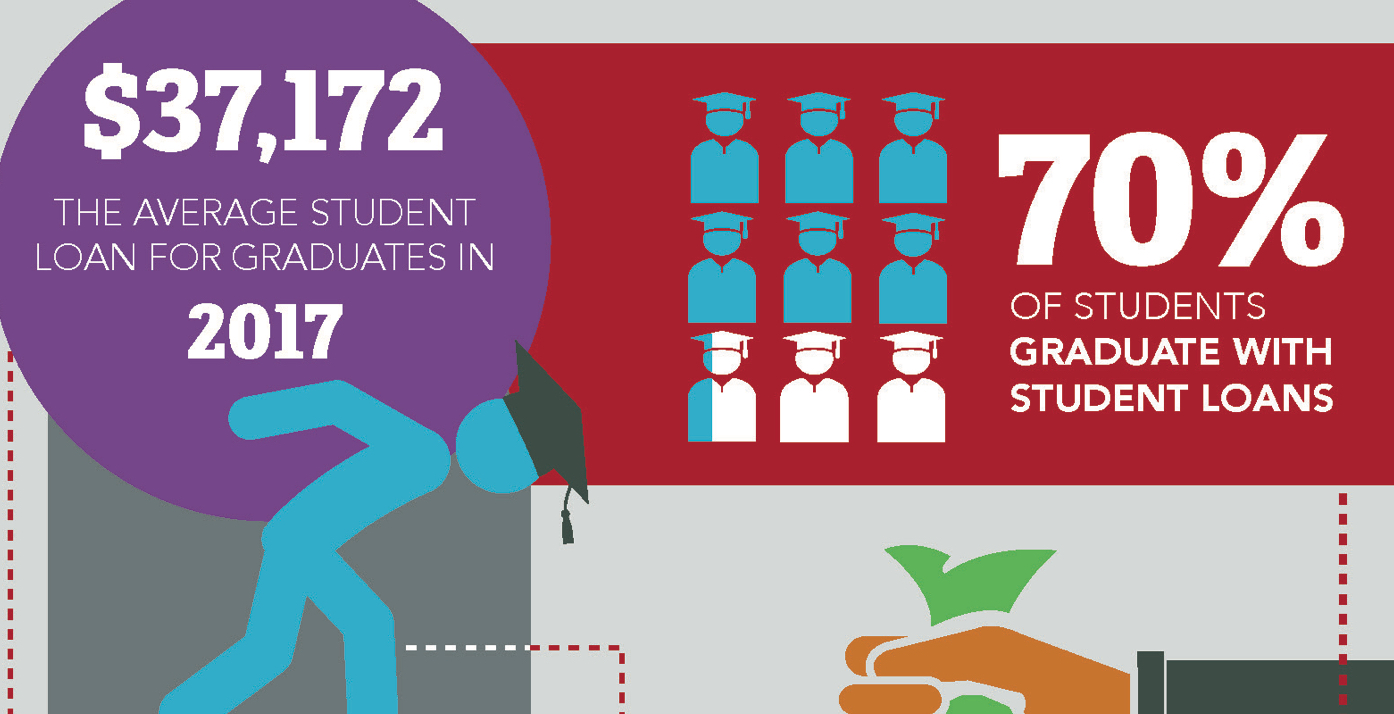

Your child’s college fund.

It’s never too early to start saving for college. A 529 plan has tax advantages but requires you to spend the money on qualified education expenses or pay a penalty. For greater flexibility, talk to a financial advisor about setting up an investment or savings account specifically for college savings.

Your daycare provider.

These can fill up quickly, and you may find that pre-paying for childcare while you’re still waiting for the baby makes sense.

Your family values.

Having a child means you’ll be passing on your values, including how you regard money, spending, saving, and wealth. Remember that your child will learn from your financial habits!